Since the US Securities and Exchange Commission (SEC) proposal in March 2022, public companies are expecting to begin reporting their carbon emissions and reductions progress alongside their financial results. Cority is covering the progress of the proposal and has produced a series of resources on what to look out for ahead of the final vote.

This article covers the key takeaways on the SEC new proposal. It also provides answers to some frequently asked questions and how Cority’s software can help start preparations.

Key Takeaways On The SEC’s Proposed Rule

This proposal is part of a much larger global movement, as international Governments are demanding more transparency and more climate action. It is clear that the regular disclosure of emissions and reductions plans is here to stay. While some of the new reports required by the SEC may not be due until 2024, many companies aren’t waiting to get started. Many investors are asking for the climate data now, and companies that have it and can manage it easily with software – such as Cority’s Sustainability Performance Management software – will both be able to answer those questions and get a head start on what’s to follow.

This new ruling will help to centralise climate risks in decision-making for companies. It is also driven by the demands of shareholders and investors for companies to consider climate reporting as a smart business decision. If you are a public company, you’ll need to start preparing to meet the proposed SEC disclosure requirements. But keep in mind that even if you have a private company, you’re competing against public companies who will need to meet these new requirements, in a marketplace that increasingly expects ESG disclosures from businesses. Therefore, while the takeaways mostly apply to public companies, all companies should give them strong consideration.

Get Organised

Your company may already be conducting an internal analysis of their GHG emissions and their materiality to business or may have publicly announced GHG reduction goals. If so, you already have a good foundation to build on to facilitate public sharing of metrics and details they already track internally.

Expect More Focus on ESG

More stakeholders, including regulators, investors, and members of the general public, are demanding accountability and transparency when it comes to ESG. The SEC is likely to continue to expand its concept of materiality and its disclosure requirements.

Improve Your GHG Management

Many organisations struggle to report GHG emissions, especially Scope 3. Cority’s software solutions can simplify this task by providing a common platform for tracking all three scopes of GHGs and aligning your reporting with common disclosure frameworks.

FAQs:

How will the new rule affect how we calculate carbon footprints?

The SEC rules almost entirely align with the GHG Protocol. It is unlikely that you will have to change your existing approach to emissions if you are already calculating your emissions and using this methodology. However, we advise that you check whether your current Scope 1 & 2 emissions boundary, as well as your Scope 3 emissions, includes all entities in your consolidated financial statements. This will help to future-proof your footprint and better align it with your financial reporting.

Does the proposal include an auditing requirement?

The proposal includes an auditing requirement from a neutral, trusted, and experienced third party covering, at a minimum, the disclosure of the company’s Scope 1 and Scope 2 emissions (everything except Scope 3 disclosures). Third-party attestation auditing requirements will phase in over two years. Additionally, they will only apply to accelerated filers and large accelerated filers. This report should also include related disclosures about the attestation service provider. We see this as “limited” assurance of the ESG information being disclosed. This is less strict than a financial audit. However, it still requires working with a sustainability reporting partner organisation.

What stage is the proposal at?

The SEC’s initial proposal is currently open to a public comment period until June 10th, 2022. It will then review those comments and incorporate them into the final draft. If adopted, the rules will then go through a phase-in period. This would require disclosures in filings made as early as 2024 for information in the 2023 fiscal year. The expectation is that the rule will pass in 2022, and be applied for 2023 (and beyond) reporting years.

Once the proposed SEC ruling is finalised, when would we need to comply?

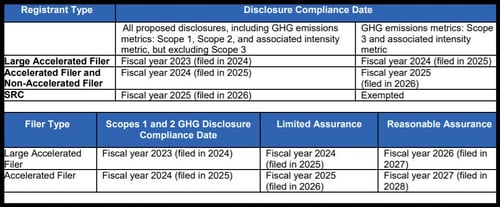

The proposed SEC rules include preliminary dates for compliance between 2023 and 2025, dependent on reporting company size. For size definitions and associated compliance timeframes see the chart below from the SEC’s fact sheet that summarises the proposed timeline.

Should we wait to disclose emissions and/or targets until the SEC ruling is finalised?

- We do not recommend delaying the measurement and disclosure of emissions or emissions targets. The proposed SEC rules closely align with current best practices.

- Alignment is a goal of the SEC to reduce the cost of compliance. This is unlikely to change in the final rules.

How Cority’s Solutions Can Support Carbon Disclosure For SEC

Cority’s Sustainability Cloud provides an integrated approach to addressing the challenge of both climate risk as well as Scope 1,2 and 3 emissions calculation and reporting. Cority’s Sustainability Performance Management software enables users to monitor Management Information and collect, analyse and report site-level climate change risks and opportunities. This will likely be aligned with the new SEC reporting requirements.

Providing a central hub for the collection and aggregation of Scope 1, 2 and 3 data and across all 15 Scope 3 categories, Cority’s solutions support businesses on their climate reporting journey and will adapt as the SEC requirements come into fruition.

References

SEC Proposes Rules to Enhance and Standardize Climate-Related Disclosures for Investors – SEC

A Guide to the SEC’s Proposed Climate Disclosure Requirements – SEC

The SEC Unveils Proposed Climate Disclosure Rules – ESG Today

Comprehensive Analysis of the SEC’s Proposed Rule on Climate Disclosure Requirements – Deloitte

Continue reading

Understanding the SEC’s new carbon disclosure recommendations – Cority