With the Green Deal, the European Union not only wants to send a signal, but is also putting an ambitious plan for sustainable transformation into concrete terms. The EU Taxonomy and the Corporate Sustainability Reporting Directive (CSRD) are key instruments to direct capital into sustainable economic activities and increasing transparency about sustainability performance. Below we will answer some key questions we regularly encounter about these two instruments.

A Green Deal as an Ambitious Framework

The European Green Deal is a transformation and growth plan which aims to decouple the European Union’s economic growth from resource use. On January 14, 2020, the European Commission presented the European Investment Plan for this Green Deal with the objective to mobilize at least 1 trillion euros in sustainable investments over the next ten years.

Not least through the Investment Plan, the Green Deal addresses core problems such as the lack of a definition for sustainable investments and the high risk of greenwashing. Plus, it looks at the lack of comparability and availability of sustainability data demonstrating relevant corporate performance.

The EU Action Plan on Sustainable Finance is considered to be the central support for the European Green Deal, which was presented at the end of 2019 and will steer private investments to transition toward a climate-neutral economy. This is exactly where the EU taxonomy and the sustainability reporting obligation (old: NFRD; new: Corporate Sustainability Reporting Directive) step in.

The EU Taxonomy: Classification for Sustainable Investments

The EU Taxonomy is a classification system to clearly define sustainable investments and respective economic activities that contribute to the EU Green Deal. This classification will provide guidance to financial actors to make it easier to channel capital into demonstrably sustainable investments.

The EU Taxonomy – as it currently stands – considers the following six goals:

- Mitigate climate change

- Adaptation to climate change

- Protection of water and marine resources

- Transition to a circular economy

- Pollution prevention and control

- Protection and regeneration of biodiversity and ecosystems

The idea is for each of these six goals to define the technical screening criteria, KPIs, and thresholds to declare that an economic activity of a specific sector is taxonomy aligned. So far, criteria have been developed for “mitigate climate change” and “adaptation to climate change.” Criteria for the other four environmental goals will follow.

In addition, the current status of the Taxonomy Regulation focuses on specific sectors and their economic activities, namely the following:

- sewage, water, waste

- education

- construction & real estate

- energy

- finance & insurance

- forestry

- health & social issues

- information & communication

- art & entertainment

- manufacturing

- transportation

- environmental protection

- scientific & technical activities

How the EU Taxonomy Works

To be EU Taxonomy aligned, an economic activity must contribute significantly to one of the six defined goals above. Additionally, it must not significantly affect any of the other five goals. And since the EU Taxonomy currently focuses exclusively on the six environmental goals, compliance with minimum requirements according to the OECD Guides on Multinational enterprises and UN Guiding Principles on Business & Human Rights is required as well. These three spheres, “substantial contribution,” “do no significant harm,” and “minimum safeguard,” must be positively assessed or answered for an economic activity to be considered aligned with EU Taxonomy.

The extension of the Taxonomy to include social aspects and additional classification levels is currently in discussion.

One Article Brings Together Corporate Sustainability Reporting Directive and EU Taxonomy

Article 8 of the Taxonomy Regulation will increase transparency in the market and help prevent greenwashing by providing information to investors about the environmental performance of assets and economic activities of financial and non-financial undertakings.[1]

Thus, the taxonomy will impact real economy companies. First of all, it will affect companies that are already required to report non-financial information under the Non-Financial Reporting Directive (NFRD). These will be subject to additional disclosure requirements in 2022 for the reporting year 2021. Later, the Corporate Sustainability Reporting Directive (CSRD) will expand the circle of those affected by a significant factor.

The NFRD, since 2018, has required many companies to report on non-financial aspects of their business such as environmental protection, social responsibility, respect of human rights, anti-corruption, and bribery. This reporting obligation (NFRD) is now being revised due to Article 8 of the Taxonomy Regulation and an adapted proposal has been developed under the name “CSRD.”

The CSRD will replace the NFRD in the future. The CSRD will come into force in 2024, so that companies will have to report in accordance with it for the first time for the 2023 financial year. In 2022 – based on existing standards (such as GRI and Co.) – a uniform reporting standard is to be published by the EU, according to which reporting is to be carried out. This standard will initiate more in-depth reporting, align how corporations in the real economy report on sustainability, and how financial market players approach ESG.

The scope of the reporting obligation will be significantly expanded. Where previously only large companies of public interest with more than 500 employees (e.g., capital-market oriented companies, banks, and insurance companies) were subject to the reporting obligation, the CSRD will affect all companies that meet two of the following three criteria:

- 250 employees and/or

- 40 million euros turnover and/or

- 20 million euros in total assets

This means that instead of the current 11,700 corporations, almost 50,000 companies across the EU will be subject to reporting requirements and will also have to demonstrate their taxonomy compliance. The CSRD also extends the reporting requirements. In the future – in addition to the existing requirements – double materiality will need to be integrated in the management report.

Additionally, reports will need to contain future-oriented information such as goals and indicators and will need to be digitally extractable in a format like XHTML. Finally, limited assurance of the reports will become mandatory three years after the CSRD comes into force.

Common Questions About Corporate Sustainability Reporting Directive and EU Taxonomy

Let’s look at a few frequently asked questions that have reached us recently:

What are the implications and conclusions if a company is not taxonomy-aligned with its economic activities?

When evaluating a company’s activities, if one concludes that an activity is not aligned with the Taxonomy, there is currently no immediate sanction. However, one should think about how to get this activity aligned with the Taxonomy in the future in order to be attractive to the financial market.

As well, aligning one’s own economic activities with the Taxonomy will provide value in the form of a deeper understanding of one’s own sustainability performance, attractiveness to the financial market, as well as the future knowledge of one’s own impact on the environment, climate, and society.

How can a company best prepare for the upcoming requirements of the EU Taxonomy and/or CSRD?

Companies can prepare themselves for the upcoming requirements by establishing processes, data management, and a robust documentation of decisions regarding their own sustainability performance. Because, ultimately, this will be the basis for answering the EU Taxonomy and being compliant with the CSRD.

Which specific reporting standard is recommended in preparation for upcoming requirements?

This depends on the maturity of the company in terms of sustainability and reporting. The GRI standard is a good start for many companies, as it is holistic and approaches the relevant sustainability topics via double materiality. If your company is further along in your sustainability maturity journey, a standard that helps integrate financial and non-financial aspects in one consistent and coherent document may be of value.

According to the GHG Protocol, it’s also advisable to prepare a solid carbon footprint because the EU Taxonomy expects concrete information on the climate impact of a company’s activities through the first two goals.

What impact will the EU regulations (EU Taxonomy and Corporate Sustainability Reporting Directive) have beyond Europe in the rest of the world?

At this point, it’s still highly speculative how this regulation will affect the rest of the world. But in the past, we’ve seen European standards become a worldwide benchmark. Experts are anticipating we’ll see a new dynamic around sustainability performance and reporting.

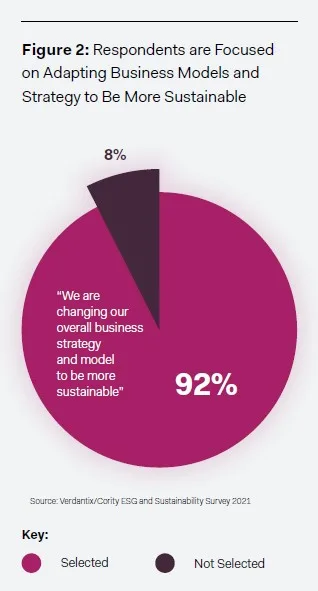

Cority recently engaged with independent research firm Verdantix to conduct a study, The Way Forward for ESG: Firms Are Adapting Business Strategy and Boosting Technology Investment, that found that 92% of firms are adapting their business strategy and model to be more sustainable.

Moreover, it’s well known that globalization is turning the world into a village where market mechanisms are moving closer together.

Sustainability Software Solutions as a Central Cornerstone

As companies begin adapting to meet the requirements of the EU Taxonomy and the Corporate Sustainability Reporting Directive, external auditing will become essential, which is why managing data accurately and efficiently is becoming a critical need.

Decisions and changes in sustainability management must be comprehensible and transparent to a third party. In addition, as the need for more granular data expands, larger volumes of data are being collected, which then needs to be aggregated – not always an easy task to handle manually without introducing errors.

Sustainability software solutions can play a central role in helping meet these goals. To do this, you need a resilient software system that supports you and checks plausibility, thus reducing errors. Check out our guide, Finding the Right Technology in a New Era of Sustainability for more info on what to look for when considering sustainability software to help navigate common sustainability reporting challenges. Improving sustainability performance and demonstrating the accuracy of the information to meet requirements will call for data-driven insights that software can help companies uncover.

Still have questions on EU Taxonomy or Corporate Sustainability Reporting Directive?

Watch our webinar on this topic or reach out to us, and we’d be happy to have a conversation.

[1] Regulation (EU) 2020/852 of the European Parliament and of the Council of 18 June 2020 on the establishment of a framework to facilitate sustainable investment and amending Regulation (EU) 2019/2088 (OJ L 198, 22.6.2020, p. 13–43).